Block#3: Neobanks vs Crypto Wallets in 2025 - Overlapping Consumer Finance & the Future of Digital Banking

Thinking in Blocks: Where Web3 meets the real world insights on AI, Stablecoins, and the Onchain economy

Introduction - The Great Convergence?

In 2025, two previously distinct product categories in consumer finance are converging:

Neobanks: scaled platforms optimized for regulation, fiat infrastructure, and multi-market distribution.

Crypto-native wallets and apps: systems built for onchain access, programmable money, and composable protocols.

Historically, these products targeted different users and operated under various constraints. Neobanks focused on trust, compliance, and fiat-centric flows. Crypto wallets emphasized control, speed, and decentralization. In recent months, these boundaries have begun to erode.

Recent moves reflect this shift:

Kraken launched Krak, a consumer app with staking, global transfers, and yield.

Revolut is integrating Lightning payments and building a native stablecoin.

Robinhood announced it will offer tokenized U.S. equities to EU users, tradable 24/5, and is building their Layer 2 in partnership with Arbitrum

These are responses to shared market changes:

Regulatory frameworks are maturing (MiCA, GENIUS Act).

Onchain infrastructure is increasingly scalable and developer-friendly (Layer 2s, modular stacks).

Stablecoins have become credible financial primitives, moving trillions annually.

Wallet UX has improved, removing barriers to mainstream use.

For crypto apps, staying crypto-native caps user acquisition and retention. For neobanks, remaining fiat-only is a structural limitation. Both are now building toward integrated financial surfaces, where custody models, asset types, and settlement layers are abstracted behind a seamless user experience.

It is a realignment of priorities across infrastructure, compliance, and user experience driven by the same strategic imperative: scale.

Web2 Neobanks: UX Maturity Meets Infrastructure Constraints

Neobanks and traditional fintech players, such as Revolut, N26, Wise, and SoFi, have redefined digital banking over the past decade. Their success stems from a combination of polished mobile-first UX, licensing agility across multiple jurisdictions, and efficient global distribution. For millions of users, these apps serve as comprehensive financial platforms, covering daily payments, savings, foreign exchange, investing, and crypto offerings.

The underlying business model is also well-established: a mix of interchange fees, subscription tiers, and monetization of wealth and lending products. This combination of functionality, trust, and convenience has allowed neobanks to scale rapidly and build strong brand affinity.

Structural Limitation: Legacy Rails

However, these platforms remain tightly bound to traditional financial infrastructure. Payment and settlement flows continue to run through legacy systems, including SWIFT, SEPA, ACH, and card networks. These systems introduce friction, particularly when expanding into programmable services such as real-time remittances, tokenized assets, or smart contract-based treasury management.

Today, these platforms cannot support instant settlement, dynamic yield routing, or onchain programmable credit without relying on external middleware or expensive workarounds. That makes them seem increasingly ill-suited to power the next generation of financial experiences, or so it would appear.

Strategic Options: Expansion vs. Infrastructure Shift

Some neobanks are expanding their reach through geographic expansion or by layering on adjacent verticals, such as credit, insurance, and business banking. Others are beginning to explore integration with Web3-native infrastructure to support faster settlement, open asset standards, and programmable flows.

Competing at the infrastructure level, particularly in a market moving toward real-time, composable financial products, will require a fundamental shift in how money moves through these platforms.

In the sections that follow, we’ll delve deeper into how Revolut and Robinhood, a broker-dealer that is increasingly overlapping with neobank territory, are approaching this infrastructure shift, each from a different origin, yet with converging strategic intent.

Revolut

Revolut: Strategic Positioning in Regulated Crypto Infrastructure

Revolut has expanded its approach to crypto from access (i.e., brokerage) to infrastructure. What began as a retail trading feature has evolved into a vertically integrated product line, embedded across FX, savings, card spending, and broader financial services. Users can buy, stake, transfer, and pay with over 230 tokens, all inside the same interface that powers their fiat-based activity.

The company’s 2024 results validate this expansion. It closed the year with 52.5 million users, up 38% from 2023, and reported £3.1 billion in revenue a 72% increase year-over-year. Pre-tax profit reached £1.1 billion, a 149% jump. The Wealth segment, which encompasses both equity and cryptocurrency trading, generated £506 million, representing a nearly 300% year-over-year increase. While crypto-specific figures were not broken out, Revolut cited trading activity, including crypto, as a key contributor to this growth.

Infrastructure and Execution Leverage

In 2025, Revolut began building infrastructure that enables control over core financial rails. The most strategic piece is its native stablecoin, currently in development, which is expected to support real-time internal FX conversion and settlement. This could unlock direct margin capture on cross-border flows and reduce reliance on card networks for backend clearing.

At the same time, Revolut integrated the Bitcoin Lightning Network via Lightspark, enabling real-time BTC payments across the UK and EEA. This reduces transaction costs and latency compared to traditional networks, positioning Revolut to support crypto-native flows within a familiar user experience. Additionally, a fiat-to-wallet ramp was introduced, enabling users to transfer balances directly to external custody, extending the utility beyond closed-loop trading and into user-directed asset mobility.

These are architectural decisions that give Revolut the flexibility to build programmable financial products without being constrained by the limitations of legacy infrastructure or third-party crypto service providers.

Regulatory Positioning as Strategic Moat

One of Revolut’s most significant advantages is its favorable regulatory position. It holds a full UK banking license and a crypto registration with the Financial Conduct Authority. This enables it to offer fiat and digital asset services under a unified compliance framework, removing the need to fragment flows across separate legal entities or vendors. For end-users, it means a seamless user experience across both fiat and crypto rails. For Revolut, it means higher velocity for product development and lower compliance overhead per unit of feature shipped.

In a market where many wallets and fintechs operate under narrow or fragmented licenses, this is a structural differentiator, especially for launching stablecoins, offering crypto-backed payments, or embedding yield into mainstream financial services.

Institutional Expansion and Product Depth

In Q1 2025, Revolut began hiring for a general manager to build out a crypto derivatives business, with roles based in London, Barcelona, and Dubai. The positioning is deliberate, the EU, under MiCA, and Dubai’s VARA regime both offer licensed frameworks that permit institutional or professional-grade derivatives. Revolut is likely to start there, building out backend infrastructure and compliance layers that allow institutional flows to scale without conflicting with UK consumer restrictions. This move complements the broader infrastructure strategy. It enables Revolut to tap into new capital sources beyond retail flows while deepening its presence in digital asset markets.

Market Position and Execution Risk

Compared to its peers, Revolut is outpacing them in terms of infrastructure scope. Wise continues to focus narrowly on fiat remittances. N26’s crypto product remains minimal and partner-based. Robinhood is expanding its presence in tokenized equities and Layer 2 rails, but its core model remains centered on retail investing. Revolut, in contrast, is moving toward infrastructure consolidation, encompassing asset custody, FX, crypto liquidity, and now derivatives—all under one unified UX layer and with a single compliance surface.

That said, execution remains the key variable. The stablecoin’s rollout will depend on regulatory clearance, particularly in the UK and EU. The wallet ramp’s usage and transaction volume will determine how deeply Revolut can own asset mobility. Institutional expansion into derivatives will require the integration of risk, compliance, and execution systems, which are non-trivial to build or scale.

Strategic Outlook

Revolut is not attempting to match Web3 composability or protocol-level access. It is building a somewhat closed-loop, regulated platform that abstracts the complexity of onchain systems while integrating their most valuable primitives: programmable money, low-cost global settlement, and custody-agnostic asset movement.

Suppose it successfully launches its stablecoin and integrates programmable flows such as cross-border settlement, FX routing, yield surfaces, and structured institutional products. In that case, it will not be competing with other neobanks solely on UX. It will operate with an infrastructure margin profile and product optionality more akin to an on-chain banking platform. What Revolut is building is control over the rails that next-generation financial products will rely on.

Robinhood

Robinhood’s latest announcements at “To Catch a Token” represent a pivotal strategic shift, positioning the company as a foundational infrastructure player in the emerging tokenized financial ecosystem. By launching/announcing to launch tokenized U.S. stocks and ETFs for EU users, Robinhood is blurring the lines between traditional and decentralized finance, offering fractional equity exposure with 24/5 access, dividend support, and zero commissions.

This makes U.S. markets more accessible to a global retail base, while also converting Robinhood’s European app from a crypto-only product into a full-spectrum investment platform powered by blockchain rails. Coupled with the reveal of its proprietary Layer 2 blockchain (built on Arbitrum), Robinhood is signaling its long-term intent to own the settlement layer for tokenized assets, enabling always-on trading, seamless bridging, and eventually self-custody capabilities that could redefine how retail investors interact with real-world financial products. The rollout of perpetual futures in the EU and crypto staking in the U.S. and EU further reinforces this strategy by appealing to more sophisticated traders while enhancing platform utility and yield potential. Layered on top are a suite of tools, including Cortex for AI-driven insights, smart exchange routing, tax-lot selling, crypto rewards via credit card, and advanced mobile charting, which turn Robinhood into a vertically integrated, crypto-native trading experience.

What emerges is a platform that caters to speculative retail users and also increasingly builds institutional-grade capabilities accessible through a consumer-friendly interface. Strategically, this positions Robinhood at the nexus of regulatory clarity, infrastructure control, and global market access, distinct from both legacy brokerages and decentralized exchanges. It’s a calculated evolution toward becoming the first truly mass-market, tokenized investment platform.

“Crypto is much more than a speculative asset. It has the potential to become the backbone of the global financial system.” - Vlad Tenev, CEO

“Introducing the Robinhood chain... to carry the entire traditional financial system into the future.” - Tanya Denisova, COO

“I want to make crypto less complex and more accessible to more people.” - Johan Kerbat, Head of Robinhood Crypto

The Robinhood Chain, its future L2, will enable asset issuance, custody, and compliance at the protocol level. This represents a shift toward internalizing control over clearing, settlement, and asset management.

Strategic Rationale: Why This Matters

Vertical integration: Moves clearing, custody, and execution in-house via Layer 2, reducing dependency on legacy intermediaries.

24/7 settlement: Enables continuous trading and instant clearing, improving capital efficiency and user experience.

Higher monetization per user: Unlocks new revenue streams through staking yield, perpetual futures, smart routing fee tiers, and premium AI features.

Regulatory scalability: Tokenized assets eliminate reliance on regional broker-dealer licenses, enabling broader, faster global expansion.

Infrastructure extensibility: Programmable rails support rapid feature deployment, AI insights, tax strategies, crypto rewards, and new asset classes.

Strategic identity shift: Robinhood is evolving from a consumer-facing brokerage into a programmable financial infrastructure provider.

Web3 Wallets & Crypto Apps: Maturing from Tools to Infrastructure

Web3 wallets have historically operated on a fundamentally different foundation than neobanks. Wallets like MetaMask, Phantom, Rainbow, Trust, and Argent weren’t initially built as traditional financial products. They were interfaces designed to manage keys, sign transactions, and interact directly with smart contracts. Compliance, user experience, and monetization were secondary.

This philosophy supported the early crypto wave. It prioritized composability, sovereignty, and multi-chain access, but it also introduced steep usability barriers. Onboarding was complex. Recovery remained brittle. Flows, such as bridging, staking, and yield farming, were fragmented and unintuitive. For crypto-native users, these trade-offs were acceptable. For the next billion, they’re not.

Strategic Repositioning: Wallets as Financial Gateways

Over the past 18 months, wallet teams have begun to reframe the problem. The goal is no longer just enabling protocol access; it’s delivering end-to-end consumer finance, spanning both fiat and crypto rails.

The global footprint underscores the need for change; a16z estimates there are between 30 and 60 million monthly active crypto users a figure derived from wallet analytics and mobile engagement data. That’s a fraction of the global financial user base. Reaching the next cohort means shifting from protocol exposure to productization.

To do this, leading teams are investing in four core areas:

Custody and recovery: Moving toward embedded recovery logic, passkeys, and social recovery models.

UX abstraction: Hiding gas mechanics, streamlining transaction approvals, and designing around fiat-denominated experiences.

Onramps and compliance: Building native KYC flows, integrating fiat payments, and deploying jurisdiction-aware transaction screening.

Platform extensibility: Enabling developers to launch wallet-based apps that abstract away raw chain interactions.

Compliance and Infrastructure as Product Strategy

This shift is reflected in how these products are designed and built. Teams are aligning with frameworks like MiCA and the GENIUS Act, embedding compliance logic directly into the architecture. In some cases, they’re acquiring licenses. In others, they’re embedding financial safeguards at the smart contract level or integrating with regulated custody providers.

Where regulation was once viewed as a constraint, it’s now a pathway to broader distribution. Compliance infrastructure opens doors to new jurisdictions, more risk-averse users, and higher-value financial use cases.

What Comes Next

Wallets are evolving from protocol gateways into infrastructure layers, reshaping how users hold, spend, earn, and interact with programmable money. Products like Krak and Ready (Formerly Argent) represent this evolution. Each targets a different surface, payments, shared wallets, and on-chain aggregation—but shares a common intent: to deliver trust, scalability, and usability without compromising composability.

Please note that several other wallets and crypto apps belong in this category, notably the Coinbase Wallet and MoonPay app, which offer robust and intuitive user experiences. However, for today’s blog, I’m focusing on Krak and Ready

The next sections delve deeper into how Krak and Ready are navigating this transition and what their design choices reveal about the future of wallet infrastructure.

Kraken’s Krak

Kraken Krak: A Consumer Stack Built on Infrastructure Control

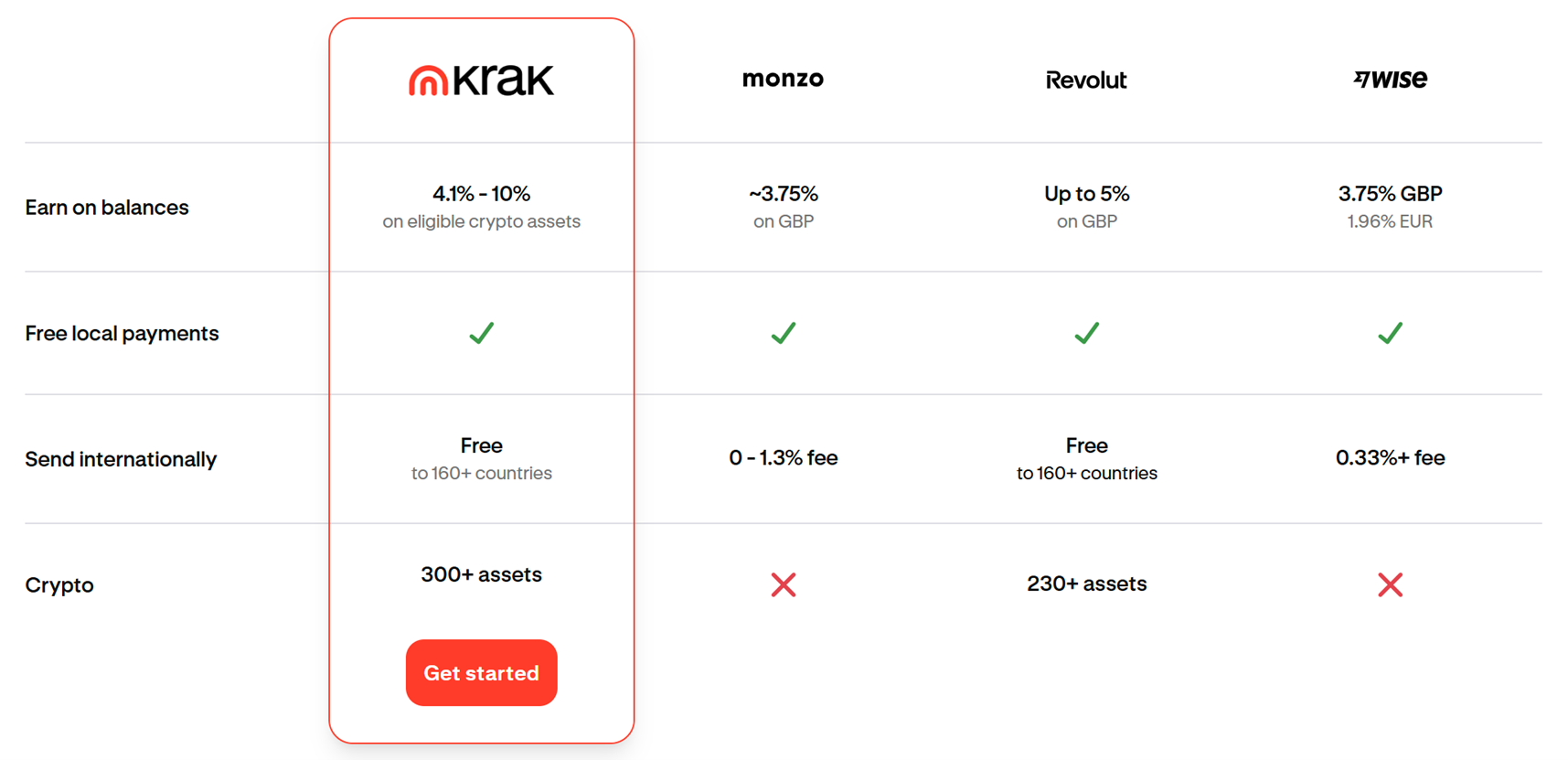

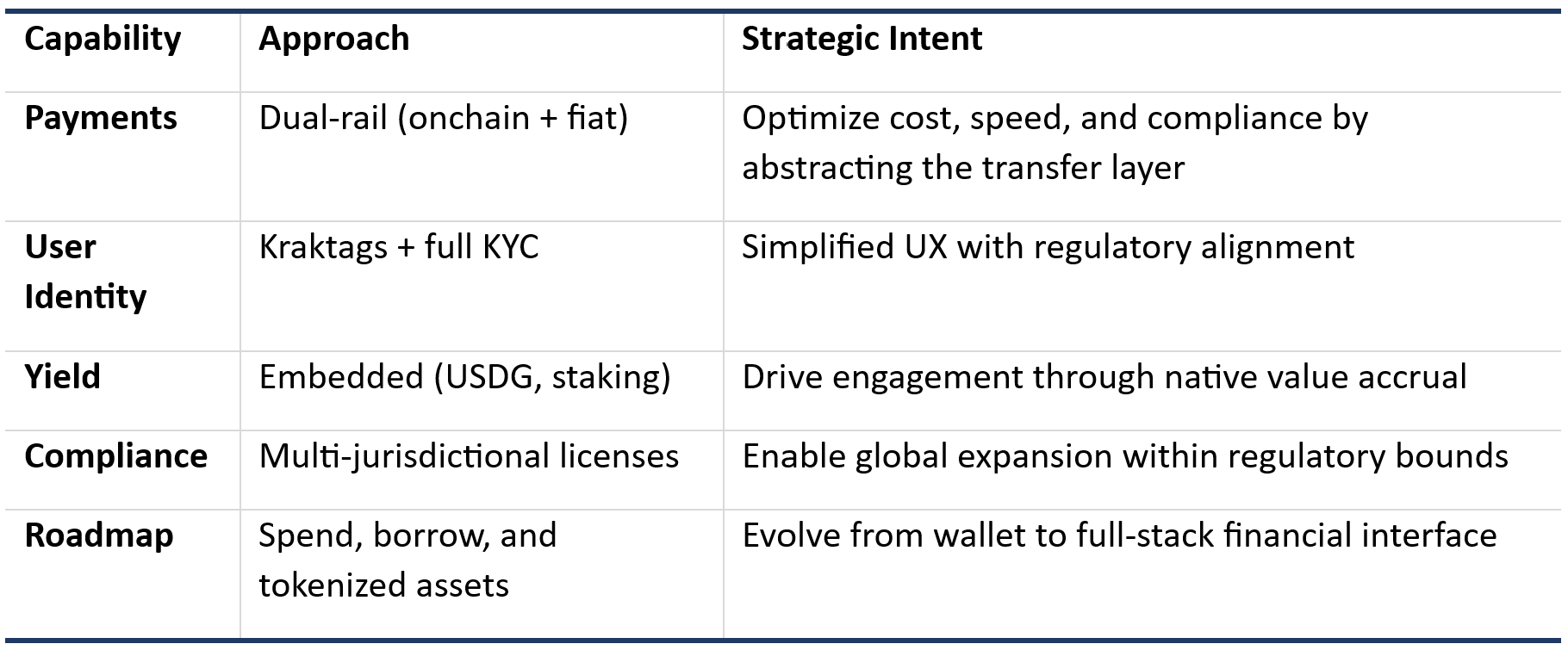

Krak represents Kraken’s shift from centralized exchange to a vertically integrated money platform. While the app offers standard features, support for over 300 assets, global P2P transfers, and embedded staking, it is best understood as an infrastructure strategy rather than a retail product release.

The design leans heavily on dual-rail architecture. Fiat transfers settle via Kraken’s internal systems, while crypto, including its USDG stablecoin, moves over public blockchains. For users, this is abstracted through “Kraktags,” which unify transfers into a single UX flow. Behind the scenes, the system dynamically routes transactions via fiat or on-chain rails, depending on the asset, jurisdiction, and speed requirements.

Yield is embedded, USDG accounts pay up to 4.1% natively, with auto-opt into staking programs where compliant. The decision to foreground passive yield reflects an intent to drive habitual usage, positioning Krak less as a speculative wallet and more as a utility layer for everyday finance.

Regulatory and Technical Foundations

Krak is underpinned by regulatory preparedness. Kraken holds licenses in multiple jurisdictions, and its MiCA-aligned operations provide a compliant base for product rollout in the EU and beyond. Identity, KYC, and recovery flows are built into the app’s architecture, enabling it to meet both compliance requirements and user expectations for mainstream financial tools.

The roadmap is expansive, encompassing card issuance, spending, lending, and tokenized assets. Each new product extends Krak’s utility, but all build on the same premise, replacing fragmented legacy rails with programmable infrastructure under Kraken’s control. What stands out is the completeness of the stack. The wallet experience is familiar to non-crypto natives, identity and recovery flows are streamlined, and the roadmap includes spend accounts, cards, borrowing against assets, and tokenized equities, showing a clear intent to expand Krak from a payments tool into a broader financial platform.

Market Entry Strategy: Building Outside-In

Krak’s initial launch spans over 110 countries, prioritizing markets with limited access to efficient cross-border payments. This aligns with a broader shift in global fintech: solving for structural gaps in dollar liquidity and remittance cost, rather than competing directly in saturated neobank markets.

The target isn’t just the unbanked (1.4 billion globally); it also includes freelancers, migrants, and businesses operating in dollarized economies with limited local banking infrastructure. For these users, Krak offers a higher trust alternative to informal cash systems, with better speed and pricing than traditional fintechs.

Strategic Framing & Product Positioning

Krak is very clearly competing in the market of everyday financial activity, backed by infrastructure that scales, compliance that unlocks markets, and a roadmap that bridges on-chain flexibility with traditional finance (TradFi) utility.

“We’re not here to rebuild the banks. We’re here to build what comes after.”- Kraken co-CEO Arjun Sethi

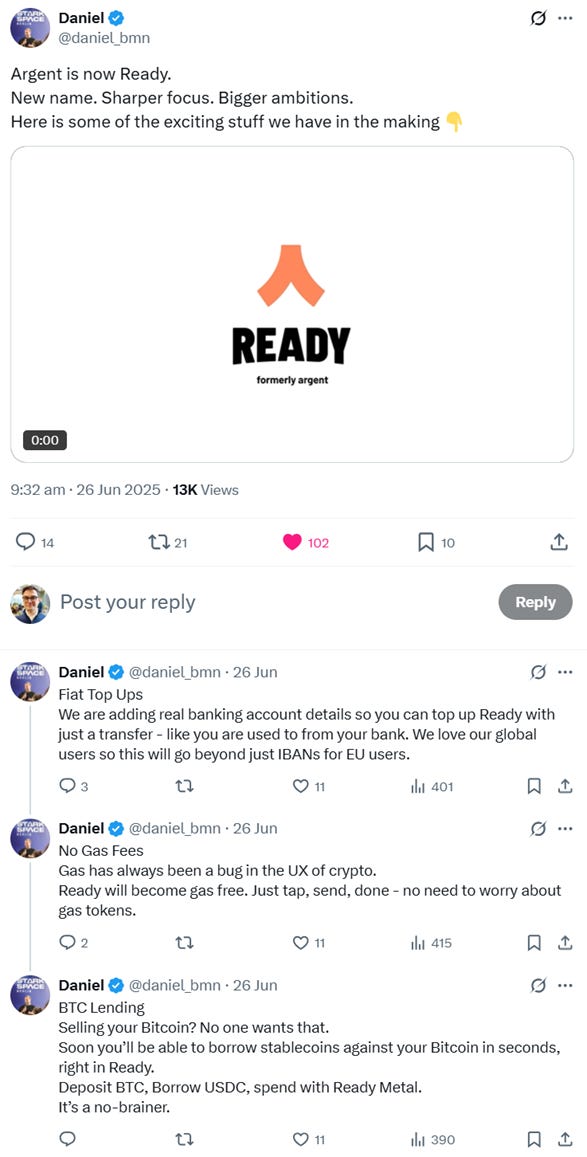

Ready (Formerly Argent)

Argent’s rebrand to Ready signals a maturation of intent. Long positioned as a smart contract wallet for crypto-native users, Argent helped pioneer secure self-custody infrastructure on Starknet. With Ready, the company feels more like a consumer-grade wallet that aims to replace the interface people use to manage their money, whether that money is fiat, crypto, or stablecoin-denominated savings.

On the surface, Ready is a clean, mobile-first wallet that supports swaps, staking, and payments, connects to Apple Pay and bank rails, offers cashback on purchases, and allows users to manage NFTs and portfolios from a single interface. However, beneath the design lies a more ambitious structural goal: to treat the wallet not as a niche tool for early adopters, but as infrastructure for everyday financial behavior.

The thesis is rooted in abstraction: most wallets still assume familiarity with keys, gas, and manual network switching. However, since as early as 2019 Argent led the charge embracing account abstraction and modular identity to eliminate traditional UX burdens of self-custody, including reliance on seed phrases Security is now handled via biometrics and two‑factor authentication. Transactions settle seamlessly through fee relayers. Now, with the rebrand of Ready, this design philosophy has been fully doubled down: delivering even smoother identity, security, and recovery experiences.

Ready stands apart through its architecture. Built entirely on Starknet with smart contract wallets, it offers features like gasless transactions, atomic batching, and wallet-level programmability.. To users, it feels like a modern financial app; under the hood, it’s fully on-chain.Strategically, Ready is notable for what it avoids: no custody, no centralized exchange, no reliance on third-party wallets. Yet it integrates with payment providers and brands to offer top-ups, cards, and real-world utility, without compromising self-sovereignty.It operates both as a consumer product and a modular wallet stack, giving it the flexibility to scale through retail adoption or partner integrations.

Why the Convergence Is Accelerating Now

As of 2025 the convergence between fintech and crypto is accelerating, driven by structural tailwinds that make crossover inevitable.

Regulatory clarity is improving

After years of ambiguity, jurisdictions are defining clear rules. Europe’s MiCA framework is now live, establishing a unified licensing regime across the 27 EU countries for the issuance, custody, and exchange of digital assets. The UK’s FCA has authorized fintechs like Revolut to offer crypto services, while U.S. lawmakers are advancing stablecoin legislation (e.g., the GENIUS Act) and beginning to outline guardrails for tokenized securities.

More firms are securing licenses

Kraken secured a MiCA license in Ireland and maintains money transmitter licenses across the U.S. Robinhood is a registered broker-dealer and crypto money transmitter. Revolut holds an e-money license and is seeking a full U.K. banking charter. Meanwhile, crypto-native firms are acquiring ATS and broker-dealer registrations to support the issuance and trading of tokenized securities. The regulatory stack is starting to look similar, regardless of which side a company started on.

Stablecoins are proving their utility

Stablecoins are now critical infrastructure. Over $27.6 trillion in stablecoin volume was transferred across blockchains in 2024, surpassing the combined volume of Visa and Mastercard. Supply growth has continued into 2025, with $247 billion in circulation as of May. USDC and USDT are widely used in settlements, remittances, and as corporate treasury rails. Fintechs and wallets are integrating stablecoins at the core: Shopify enables USDC payments via Coinbase and Stripe; MoonPay embeds stablecoin onramps; Krak uses USDG as its yield-bearing default.

Cross-border payments are going crypto-native

Remittance flows reached $860 billion globally in 2023, with average fees still over 6%. Crypto rails, particularly stablecoins, cut that to near-zero. Products like Krak, MoonPay, and SoFi's upcoming features layer fiat UX over blockchain settlement to deliver fast, cheap, and transparent transfers. For users, it's seamless.

Layer-2s unlock scalability

The Ethereum mainnet is no longer the bottleneck. Layer-2 networks like Arbitrum, Base, and Optimism handle a growing share of DeFi and payments, offering <$0.01 transaction costs and sub-minute finality. For builders, it redefines what’s possible in terms of throughput and cost. For users it means everyday payments and micropayments are now economical and cheaper than the existing non-blockchain-backed financial system.

Why hasn’t convergence happened yet?

The infrastructure is ready. In Asia, LatAm, and parts of Africa, wallets already support payments, yield, and even credit. In architecture, they outperform many neobanks, offering composability, programmable money, and real-time settlement. But despite technical readiness, global adoption remains low. The question is: why?

UX still isn’t consumer-grade

Most wallets still feel like developer tools with protocol switching, gas fees, and protocol-specific flows breaking mainstream usability. Seed phrases and browser extensions are improving, but even with account abstraction, most flows still fail to meet the expectations of fintech. If a user can open Revolut and move money in 10 seconds, why would they tolerate extra steps for onchain transfers?

Trust and recourse are missing

Users trust banks not because of UX, but because they know someone will pick up the phone. There's fraud protection, refunds, and escalation paths. In self-custody, loss is loss without human support and legal guarantees, wallets feel risky, especially for users managing meaningful capital.

No dominant brand has emerged

In the crypto world, no self-custody wallet has breached that tier. MetaMask and Phantom have gained traction, but they remain crypto native wallets. No one owns the consumer category in a way that abstracts Web3 complexity behind a familiar, trusted interface.

The value prop isn’t obvious to new users

Self-custody unlocks freedom, composability, and control, but those aren’t day-one needs for most consumers. Until wallets can deliver outcomes with higher yields, cheaper payments, and social financial tools, without a learning curve, adoption will remain limited to early adopters.

The takeaway: Wallets are competing on user experience. The core infrastructure, L2s, stablecoins, and programmable identity are here. However, product maturity, trust systems, and brand design are what will drive the following 50 million users. The convergence is about absorbing their UX lessons, distribution strengths, and compliance fluency, while retaining the core advantages of crypto: self-custody, programmable flows, and global interoperability.

That’s the unlock. And it hasn’t happened yet, but the conditions are lining up.

Product Deep Dive: What Makes a Winning Wallet or Neobank

Before diving into what makes a leading wallet or neobank stand out, it’s important to acknowledge that many core capabilities, such as self-custody, fiat‑crypto fluidity, gas abstraction, and cross-chain support, are rapidly becoming table stakes. These are now baseline expectations. Success in the next generation of consumer finance will depend on more than simple feature adoption; it will require a cohesive execution strategy, right PMF, jurisdictional coverage, licensing, GTM, brand positioning, and, above all, speed of iteration.

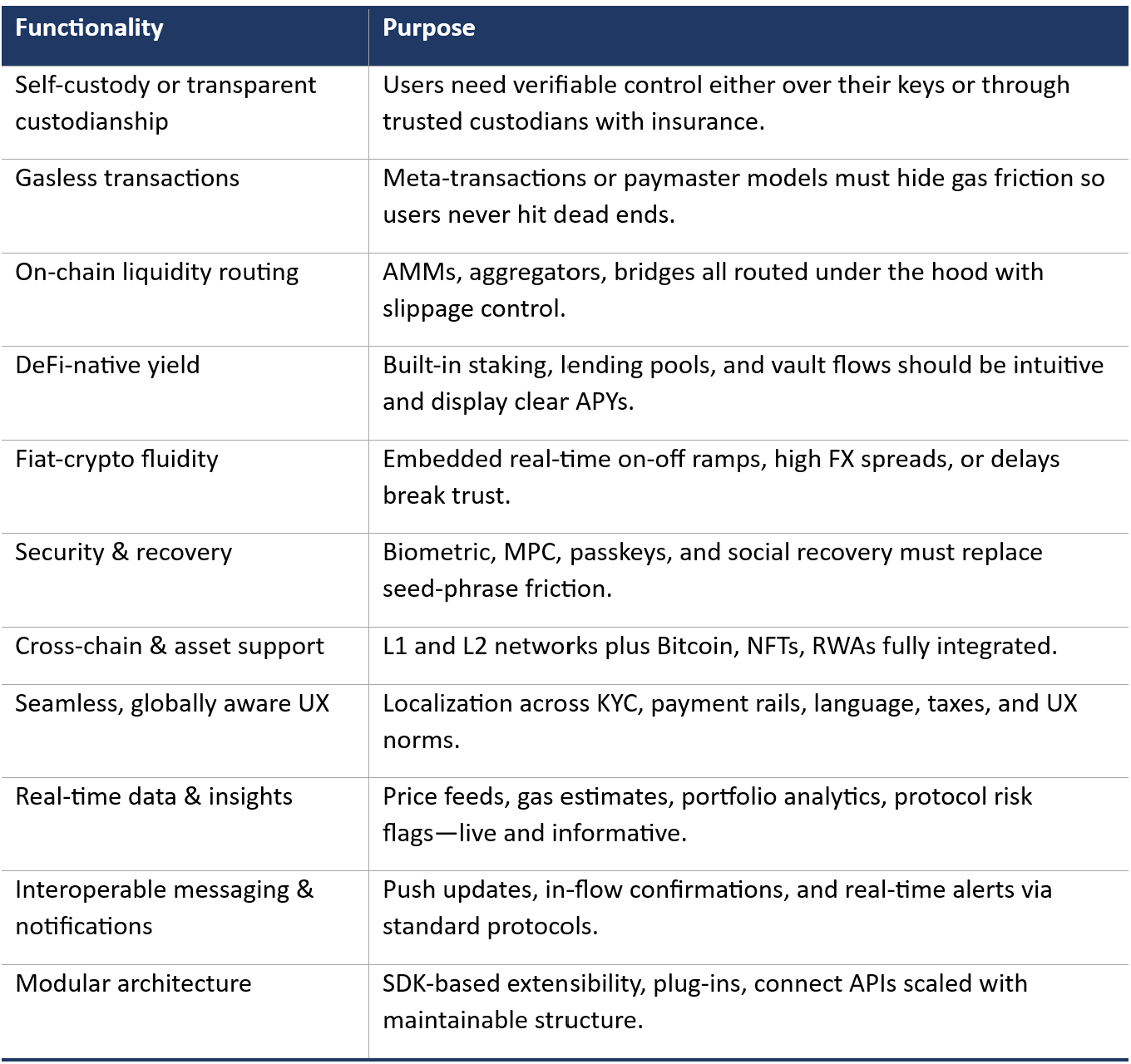

Table Stakes – The Foundation

This list isn’t exhaustive; countless design trade-offs vary by product surface and user segment, but it captures the minimum viable foundation required to compete in today’s market. In 2025, these capabilities are non-negotiable. Any wallet or neobank aiming to serve both crypto-native users and broader consumer audiences must deliver on these fundamentals. Ultimately, it comes down to three core imperatives: removing friction, ensuring trust, and enabling interoperability. Without that, no amount of innovation at the edges will matter.

Below is a snapshot of the essential capabilities any serious consumer-grade wallet or neobank must deliver:

Strategic Differentiators

Beyond the table stakes outlined above, a handful of emerging product themes are beginning to shape the next wave of wallet and neobank differentiation. A small set of startups are leaning heavily into these from day one, whether by building AI-native interfaces or embedding privacy-preserving architecture directly into the wallet. They point to foundational shifts in how consumer financial services will operate.

AI-Native Interfaces

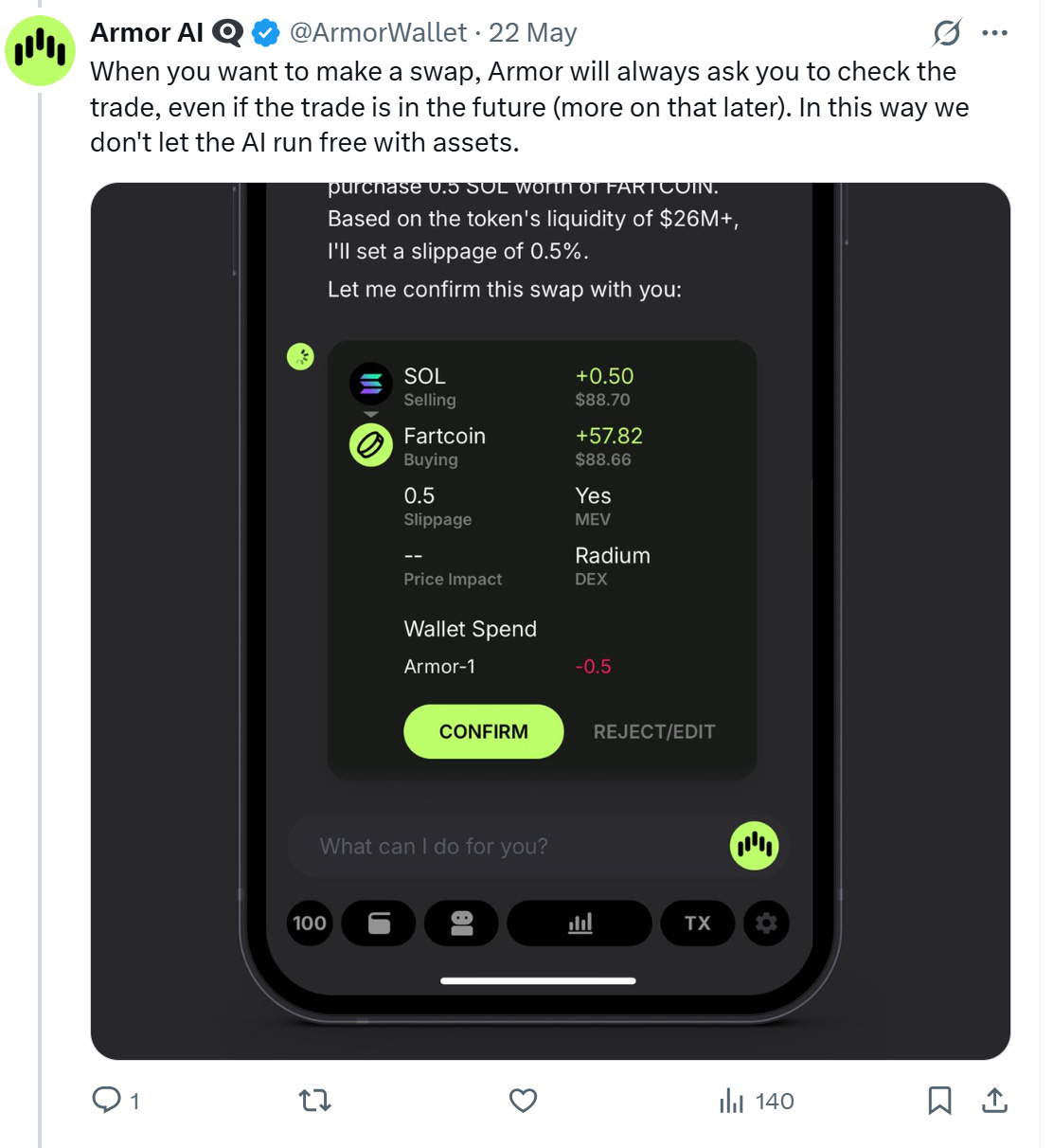

The interface layer is evolving from dashboards to decision engines. Armor is an early example of this shift: an AI-native wallet designed around conversational inputs and autonomous agents. Users engage via natural language, “DCA into ETH over three months,” “research this protocol,” and the system executes with embedded routing, compliance logic, and behavioral memory. As AI systems mature, the ability to convert intent into execution natively will shift from a differentiator to an expectation. Wallets that embed real-time insights, autonomous optimization, and behavioural context will materially outperform in terms of engagement and retention.

Integrated Identity & Privacy

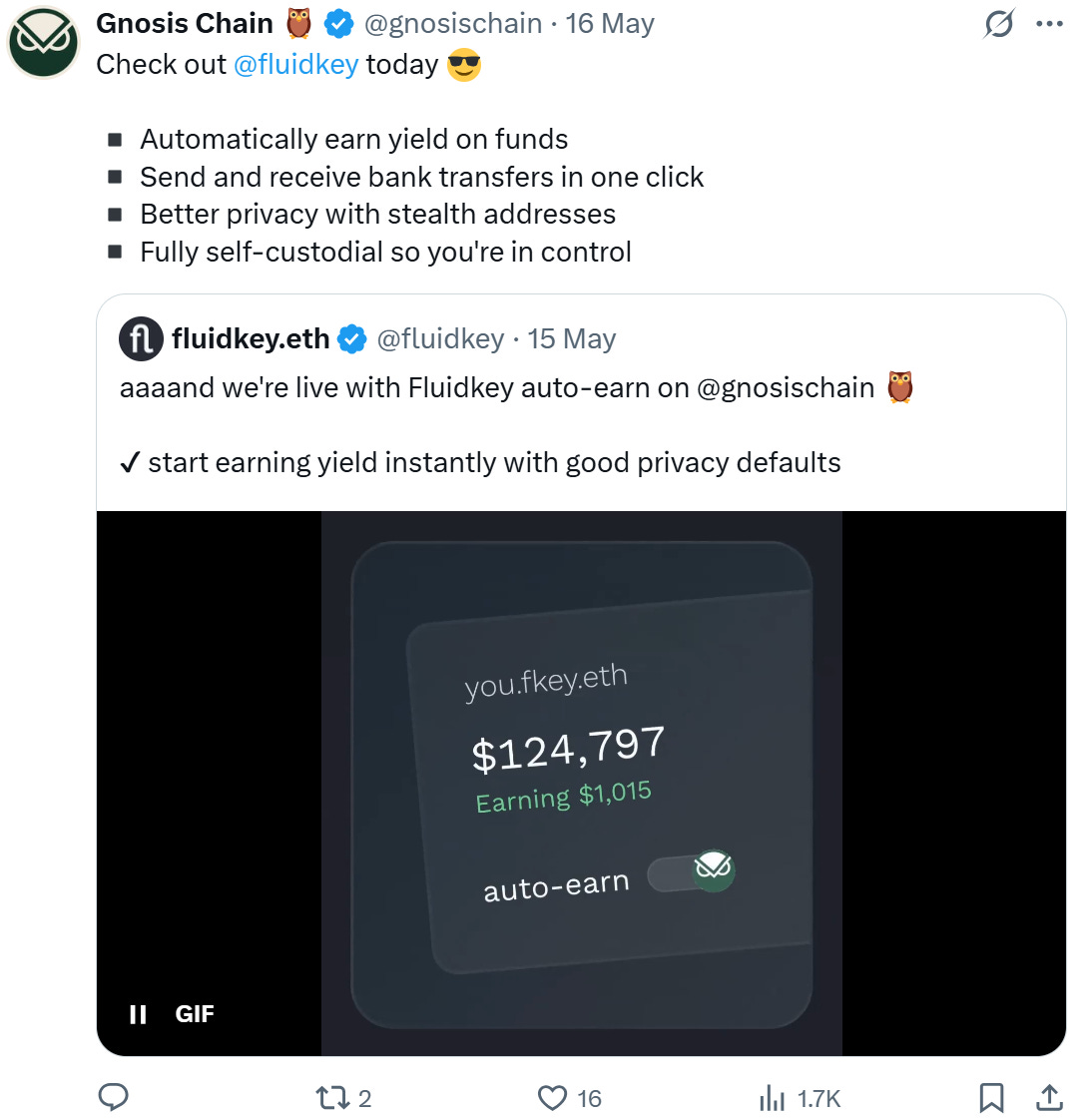

Privacy-preserving, programmable identity (biometrics, ZK credentials, wallet-bound IDs) unlocks KYC, credit, insurance, and multi-surface finance. Identity and privacy become the substrate for scale. For instance, one smart contract wallet leading the charge is Fluidkey, a self-custodial smart contract wallet focused on privacy and seamless UX. It automatically generates stealth addresses for each transaction, preserving user anonymity without sacrificing usability. Under the hood, Fluidkey utilizes ERC-4337-based account abstraction and integrates with ordinary wallets, such as MetaMask, while also offering social login via Privy. It supports fiat onramps (ACH, SEPA), automatically converts to USDC, and routes funds through yield strategies providing users with privacy, yield, and cross-chain access in one unified interface. Its emphasis on programmable privacy positions it uniquely as wallets begin competing on default user protections rather than opt-in complexity. As onchain finance expands into more regulated and high-value use cases, I expect many wallets will adopt similar models, treating privacy not as an optional feature but as a core user expectation.

Other Differentiators

Programmable Payment Logic enables core use cases, such as on-chain payroll, recurring payments, and DAO operations. Standing orders are a regular common functionality in traditional banking, but not yet common in the world of crypto wallets

Jurisdiction-Aware Compliance ensures that wallets adapt dynamically to regional requirements, a necessity for scaling across borders. For instance, a wallet automatically capturing transactional data to meet the travel rule is an obvious example here.

Shared Access Frameworks support families, DAOs, and SMBs through native multi-user controls, eliminating the need for third-party tools. Smart contract wallets would be perfect for this use case, whereby multiple parties can have rights to access an account.

Social Layer Integration increases retention by making wallets collaborative, with shared goals, contact lists, in-built social graphs, and in-app messaging that mirror the stickiness of Venmo and Cash App. Not a wallet per se, but one crypto app that stands out in this category is Vector, the social trading app.

Licensing as a Strategy unlocks product surfaces, such as tokenized equities or stablecoin settlement. Treated correctly, regulatory scope becomes product IP.

Developer Infrastructure (SDKs, embedded wallets, APIs) shifts distribution from user acquisition to integration, unlocking exponential B2B reach.

Brand and GTM Precision become decisive when product capabilities converge. Cultural relevance, narrative control, and creator alignment often determine which app wins trust.

None of these are new individually, however, the winners won’t be those with the longest feature list; they’ll be those with the most coherent system architecture. The ability to integrate identity, AI, compliance, UX, and extensibility into a single, resilient surface will separate the infrastructure layer from interface noise.

Final Thoughts

If I were building a wallet today with an eye toward long-term defensibility and ecosystem relevance. I’d prioritize two core differentiators beyond the current table stakes: privacy and intelligence. A ZK-enabled, privacy-first design is essential as wallets evolve into financial identity layers. Users need guarantees that their activity remains confidential and composable across contexts. Equally critical is embedding AI at the foundation. A wallet should learn from user behavior, surface insights across accounts and networks, and help individuals improve their financial decision-making, ultimately offering a measure of economic growth, not just balances. Looking slightly ahead, wallets must prepare for a shift where autonomous agents, not users, will drive the majority of on-chain interactions across DeFi, commerce, and payments. This means building for programmability, delegation, and intent-driven execution from the outset. The interface may remain user-friendly, but the backend needs to anticipate a world where machines transact on our behalf securely, privately, and intelligently.